Introduction

Refinancing an auto loan is a financial strategy that can yield significant savings and greater financial flexibility for borrowers. By securing a lower interest rate or extending the loan term, many drivers can lower their monthly payments and reduce overall costs. A thoughtful approach is crucial, given the long-term impact that refinancing can have on both immediate finances and future borrowing opportunities. To learn more about how refinancing could benefit your unique circumstance, review resources such as iLending for guidance on navigating the process.

Understanding the mechanics of auto loan refinancing is essential for making informed decisions. When borrowers are aware of the factors that influence loan terms, interest savings, and the consequences of their decisions, they are better positioned to maximize financial outcomes.

Understanding Auto Loan Refinancing

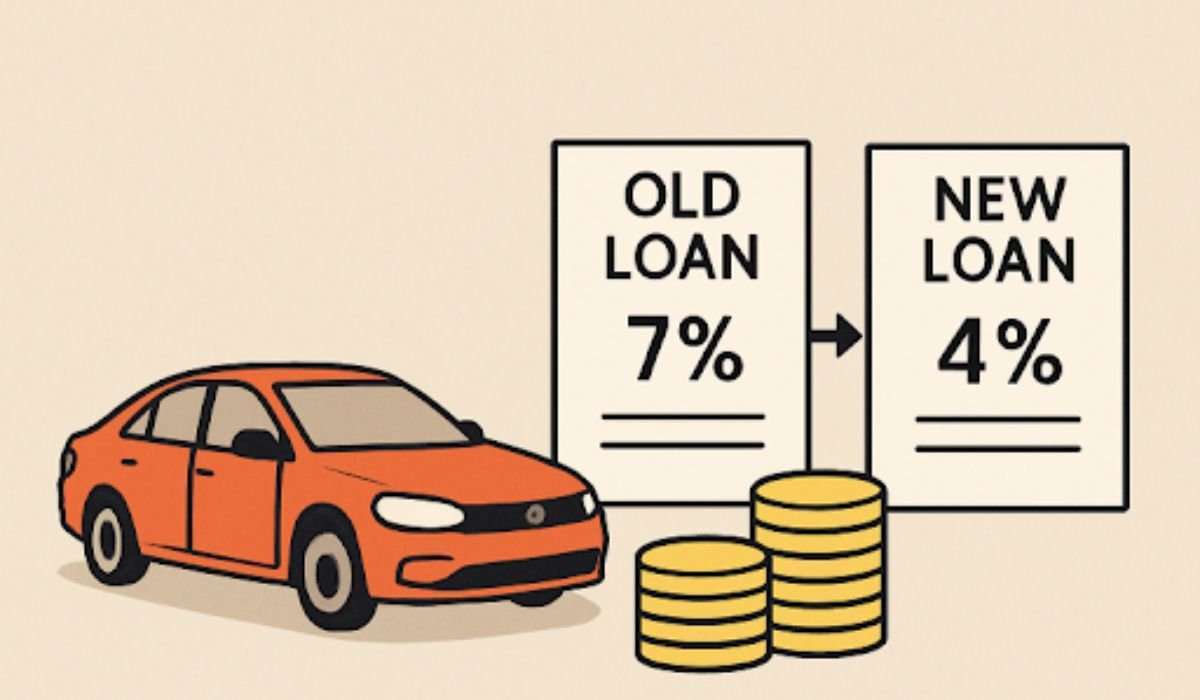

Auto loan refinancing occurs when you replace your current car loan with a new one, ideally tailored with improved rates or terms. This strategy is often used to capitalize on positive changes in a borrower’s credit profile or on a drop in prevailing market interest rates. For many, it is an opportunity to recalibrate monthly payments to better fit evolving financial needs.

Before considering refinancing, assess your financial situation and review your credit health. Lenders often reserve the best rates for borrowers with stronger credit scores, so knowing where you’re starting can help you set realistic expectations.

READ ALSO: Traceloans.com Debt Consolidation: A Full Review

Potential Benefits of Refinancing

- Lower Interest Rates: An improved credit score since your initial loan can make you eligible for lower interest rates, which translates into lower total loan costs over time. Consistently lower rates help reduce how much you ultimately pay for your vehicle.

- Reduced Monthly Payments: Extending the term of your loan lowers monthly payments, creating valuable breathing room in your budget. This is especially helpful during periods of limited cash flow, although it is important to weigh the total interest paid over the full loan period.

- Improved Cash Flow: With lower monthly payments, you may be able to redirect freed-up funds to savings, emergency reserves, or other financial goals. Enhanced cash flow increases financial resilience against unexpected expenses.

Considerations and Potential Drawbacks

- Extended Loan Term: While a longer loan term lowers each monthly payment, it typically results in more interest accruing over the life of the loan. Carefully calculate whether the immediate benefit outweighs long-term costs.

- Fees and Costs: The refinancing process often comes with upfront fees, including possible prepayment penalties on your original loan or origination charges from your new lender.

- Depreciation and Negative Equity: Since vehicles decline in value over time, lengthening your loan term can increase your risk of owing more than your car is worth. This negative equity scenario is particularly problematic if you plan to sell or trade in your vehicle before the new loan is paid in full.

Impact on Credit Score

The decision to refinance an auto loan can have several effects on your credit score:

- Hard Inquiries: When you apply for a new loan, your lender will perform a hard inquiry on your credit report. This may cause a small, temporary drop in your score.

- New Credit Account: Refinancing replaces your old account with a new one. This lowers the average age of your credit accounts, which can slightly affect your score in the short run.

- Payment History: As you continue to make on-time payments on your new loan, your payment history will improve, potentially boosting your score over time.

When to Consider Refinancing

Refinancing makes sense in several common scenarios:

- Market interest rates have dropped, making refinancing more favorable than your original deal.

- Your credit profile has improved due to a history of on-time payments or a reduction in other debts, allowing you to qualify for better terms.

- Your current payment no longer fits your monthly budget, and you need a lower monthly obligation due to changed circumstances.

Steps to Refinance Your Auto Loan

- Assess Your Current Loan: Begin by gathering details about your existing loan’s interest rate, payment schedule, remaining balance, and any associated fees.

- Check Your Credit Score: Review your credit report and score to ensure you meet lender requirements for refinancing offers.

- Research Lenders: Compare rates and terms from different financial institutions, online lenders, and credit unions to find your best deal.

- Calculate Potential Savings: Use auto loan refinancing calculators to gauge how much you could save each month, as well as overall interest paid by the end of the loan.

- Apply for Refinancing: Once you’ve selected your preferred offer, submit your application with the required documents. After approval, finalize the terms and begin payments under your new loan agreement.

Final Thoughts

Refinancing an auto loan can be a powerful tool for enhancing your financial well-being and improving your monthly cash flow when handled thoughtfully. By carefully weighing the benefits and drawbacks, understanding impacts on credit, and following a strategic refinancing process, borrowers position themselves to make confident, well-informed decisions. Those who choose to refinance in favorable conditions can reap both immediate relief and long-term financial savings.

YOU MAY ALSO LIKE: Personal Loan Myths and Facts Everyone Should Know